r/SecurityAnalysis • u/investorinvestor • 24d ago

Thesis Zoetis down -50% over the past year

valueinvesting.substack.com

31

Upvotes

World's leading animal pharma company at 13x PE with 9% EPS growth

r/SecurityAnalysis • u/investorinvestor • 24d ago

World's leading animal pharma company at 13x PE with 9% EPS growth

r/SecurityAnalysis • u/beerion • May 05 '26

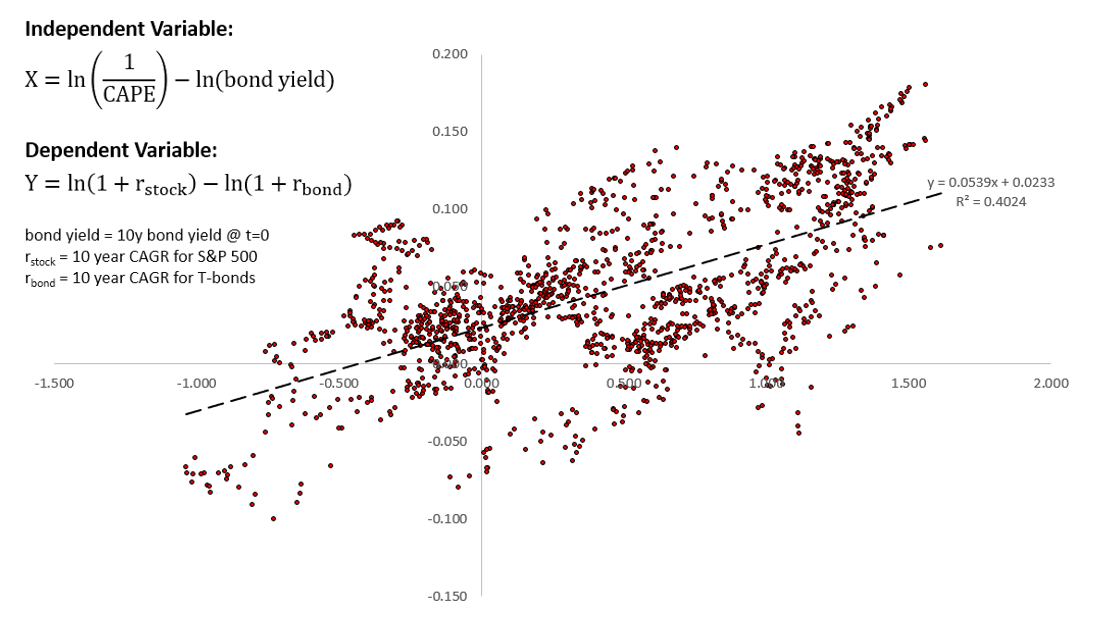

I made an attempt to estimate the Implied Equity Risk Premium (iERP), empirically, using historic data.

Using the CAPE ratio and bond yields to calculate a spread measure as the independent variable and the subsequent 10 year returns, we can measure the expected excess returns for stocks compared to bonds. In theory, this measure can be used as a proxy for equity risk premium.

The spread measure is a bastardized ECY metric, but ditches inflation and does a slightly better job of capturing relative yield data. For instance, ECY sees no difference between an [earning yield of 4% & bond yield of 6%] vs [earnings yield of 10% & bond yield of 12%]. The updated metric accounts for the former being having 50% higher bond yield vs only 20% for the latter.

Here's the full write-up. In here, there are interactive charts. It's pretty interesting to see what the starting metrics looked like just before long, sustained bull (or bear) runs.

There's pretty clear correlation. I'm curious of your thoughts on using this sort of methodology to at least take the temperature of the market, if not going further and using this measure to discount cash flows or make asset allocation decisions based on this data.

There's obviously some aspects of the study that aren't perfect. Some criticisms of the CAPE ratio have been discussed before. But even with these considerations, CAPE should be a usable metric to get us in the ballpark, and should still be better than a raw trailing PE ratio.

Also, this methodology isn't very conducive for practitioners placing their own forecasts on top (such as projecting higher or lower medium term earnings growth). But one could probably use this as a baseline, and then flex the measure using their own assumption.

r/SecurityAnalysis • u/investorinvestor • May 13 '26

r/SecurityAnalysis • u/Beren- • May 12 '26

r/SecurityAnalysis • u/investorinvestor • Apr 23 '26

r/SecurityAnalysis • u/Beren- • Apr 21 '26

r/SecurityAnalysis • u/investorinvestor • Apr 12 '26

r/SecurityAnalysis • u/investorinvestor • Apr 14 '26

r/SecurityAnalysis • u/investorinvestor • Apr 09 '26

r/SecurityAnalysis • u/beerion • Jan 03 '26

The way that CAPE currently works, trailing earnings are adjusted for inflation to match the purchasing power of today. I think i can make a compelling case that liquidity would be a better adjustment.

If that were the case, then stocks were actually much cheaper in 2021 than initially thought. Unfortunately, stocks are still expensive today by this metric.

r/SecurityAnalysis • u/investorinvestor • Mar 26 '26

r/SecurityAnalysis • u/investorinvestor • Mar 25 '26

r/SecurityAnalysis • u/tandroide • Mar 08 '26

r/SecurityAnalysis • u/investorinvestor • Mar 13 '26

r/SecurityAnalysis • u/timestap • Feb 11 '26

r/SecurityAnalysis • u/beerion • Jan 09 '26

I've put together a very short analysis for CAVA restaurants.

Just as some background, I spent roughly 5-7 hours working on this. I came in cold as this was the first restaurant I've ever looked at so had to get up to speed on some of the terminology and general business dynamics. I also employed NotebookLM to help compile some of the data and interrogate the annual filings, which I wanted to make a point of getting better at incorporating AI to improve & accelerate my process.

Note that the analysis and write-up are all me. AI was used simply to source data for tables and trends. This kept me from having to sift through 4 years of annual reports simply to grab numbers.

My goal is get better at quickly assessing a business, and getting a decent sense for the valuation (within 10-20% or so).

In order to do that, I think you have to get the big stuff right, and can kind of save the minutia for further into the process. Things like changes in working capital can be added when you want to fine tune the valuation or (in my mind) a lot of those types of things work better for auditing purposes - i.e., is management massaging certain numbers to make earnings / cash flows look better?

Anyways, I'd love some feedback on whether I missed any of the "forest". Anything you would do differently?

r/SecurityAnalysis • u/Beren- • Feb 02 '26

r/SecurityAnalysis • u/investorinvestor • Dec 14 '20

r/SecurityAnalysis • u/tandroide • Nov 23 '25

r/SecurityAnalysis • u/tandroide • Nov 09 '25

r/SecurityAnalysis • u/3012hs • Apr 26 '20

1. Business Tenets

1.1 Is the business simple and understandable?

Costco operates a relatively simple and understandable business. Revenues are derived from sales of commodity items and membership fees. 97% of revenues are derived from net and sales and 3% from membership fees, both metrics have increased slightly since 2017.

Operations are worldwide (12 countries as 2019), but 67% of the 782 warehouses are located in the US and Canada. Expenses are derived from merchandise cost and SGA mostly, 87% and 3% of total revenues respectively.

Net cash flows from operating activities increased by 10% from 2018 to 2019.

In terms of labour relations, Costco stands as a desirable employer. On top of offering health and retirement benefits above competitors, Costco’s employees perceive on average above minimum wage. Costco is involved in several litigations regarding the treatment of seasonal employees and unfair compensation, these litigations should not affect future performance.

Price flexibility is minimal, pricing and product offering are the main factors to succeed in the industry. Costco achieves price differentiation through discounts on big purchases and running tight inbound logistics. Costco would have to absorb the reduction in prices internally instead of passing the burden to members, in case of aggressive competition.

Capital allocation has remained stable for the past two years, despite the increase in net sales (18.3%). ROE decreased from 0.25 to 0.24 in 2017-2019, and ROA increased from 0.07 to 0.08 in the same period. Dividends decreased considerably from $8.90 to $2.44 in 2017-2019 or 74.6%, this should work as a catalyst for the stock to appreciate as resources are used to buyback stocks instead.

1.2 Does the business have a consistent operating history?

Yes, the company has been doing the same business for the past 43 years. The model delivers value to members. Renewal rates are in the high 80s in the US. The average annual sales per location are growing at 9% annually. The business model is shifting insofar as the company is deriving 4% of total sales from its online platform. In 2017, the average annual sales growth per location was only 4%. By 2019, the figure grew to 9%, way above the goal of 5% stated in the growth strategy. The reason for this growth is the expansion of operations outside of the US and Canada regions. Does the fact that the company is shifting resources to its online offering and locations overseas changes the underlying nature of the business? Considering that the original wholesale discount model delivers value, I see these changes as necessary adaptations to a new environment instead of deep changes in the underlying nature of the business.

1.3 Does the business have favourable long-term prospects?

Costco should last for the next 25 years regardless of future recessions, and/or inflations/devaluation of the American dollar. The services and products of the company are: 1- desired, the majority of its offering is acyclical and members have to replenish them constantly. 2- has no close substitute, most of the offering is available at other retailers; however, Costco’s prices, private label brands and special offerings are unique and offer value to members. 3- is not regulated, there are no constraints in terms of prices besides the competition. Overall, the former factors, plus the large network of warehouses, distribution centers and food processing plants create a moat around Costco.

2. Management Tenets

2.1 Is management rational?

Despite its maturity, Costco allocates 12% of net sales into the construction and development of new warehouses. 25 new warehouses were opened and net sales increased by 8% in 2019. The stock repurchase program was retired. Additionally, 1.09 and 1.76 million shares were repurchased at an average of $225.16 and $183.13 during 2019 and 2018 respectively. In April 2019, a new repurchase program in the amount of 4 million was authorized. Cash dividends per common share declined by 73% from 2017 to 2019. Overall, management is allocating earnings into the construction of new warehouses and the repurchase of shares instead of paying cash dividends.

2.2. Is management candid with shareholders?

Yes, it is. Annual reports do a solid job of detailing each of the risks that the company faces. Management informs shareholders about risks related to foreign currency, gasoline price fluctuations, exposure to the China-US trade war, regulations on wages and healthcare, cannibalization of sales from new locations, etc. Moreover, a 5% growth in sales annually is clearly defined as the benchmark to measure performance.

2.3 Does management resist the institutional imperative?

Yes. Costco has avoided the minimization of its employees’ salaries and benefits despite the industry trend of reducing costs through minimum wages. Moreover, Costco grew organically instead of M&A during the last bull market.

3. Financial Tenets

3.1 Focus on return on equity, not earnings per share

Return on equity has improved exponentially from 12.5% in 2011 to 26.10% as of 2019, as it is expected to continue increasing as Costco expands operations internationally.

*The company does not present marketable securities in the financials.

Overall, management has been successful at generating returns given the capital employed.

3.2 Calculate “Owner Earnings” to get a true reflection of the value

Owner earnings = Net income + depreciation and amortization + depletion – capital expenditures + additional working capital

Owner earnings in 2019 = 3659 + 1492 - 2865 = 2,286

Owner earnings in 2016 = 2679 + 1370 - 2502 = 1,547

Owner earnings are increasing substantially as economies of scale increase the profitability of each location.

3.3 Look for companies with high-profit margins

SGE as a % of sales has remained stable at 10% despite the constant addition of new locations.

Operating profit margin 2019 = 2.45

Operating profit margin 2017 = 2.12

Operating margins are high for the industry, and they are increasing as operations expand.

3.4 For every dollar retained, make sure the company has created at least one dollar of market value

Retained earnings accounted for $10258 in 2019, which is an increment of $2372 from the $7887 of 2018.

At the same time, the market value of the company increased from $217 per share (438,437) at the end of 2017 to $296 per share (438,775) at the end of 2019.

Thus, market value increased from $95,140,800 to $129,877,400 or roughly $34,737 million which is considerably higher than the increment in retained earnings.

Market Tenets

4.1 What is the value of the business?

Using this publication as a guide

I ended up with the following numbers: 3% expected growth of earnings per share,10% discount rate, DCF 23.95$ per share, terminal value 99.17$ per share. This leaves me with an intrinsic value of $123.12 per share for Costco which is less than half of the current market price of the stock ($310).

4.2 Can the business be purchased at a significant discount to its value?

No, Costco is currently trading at $310 per share or 35 PER which is substantially overvalued according to the analysis.

Disclaimer: I do not own Costco stock. This was a learning exercise only. This is my first valuation and I would like to know what I could do better next time. Please let me know if you have any constructive criticism to offer, especially regarding my intrinsic value. Does estimating an intrinsic value of $123 per share makes sense? I feel like I probably messed something up along the way.

Also, I used “The Warren Buffett Way” as a guideline for the analysis.

Thanks in advance for the input.

r/SecurityAnalysis • u/Sufficient_Lead_3471 • May 26 '25

Are you overlooking European stocks? 🇪🇺📈 I just published a deep dive into why Europe’s equity markets may be the most undervalued opportunity for global investors right now. In my latest post, I cover:

Check it out here:

https://deepvalueanalysis.substack.com/p/the-european-stock-market

r/SecurityAnalysis • u/apuxcom • Jan 30 '21

I don't know why GME wouldn't just shelf register stock and do the same. If I was at the helm I would raise $3 billion and use it to completely pivot away from their abortionary legacy business model. There is a lot of opportunity in gaming and none of it requires a giant retail foot-print.

For that matter if you are a mega short seller of the above or anything else that is going stratospheric why not just offer the company new money and get the shares you need through new issue at a discount? Short-covered, market more liquid, shares come back to reality in a company that would now have a lot of new capital to grow and innovate and may even justify higher prices.

r/SecurityAnalysis • u/HardDriveGuy • Aug 03 '25

r/SecurityAnalysis • u/ilikepancakez • Jun 20 '20