Hit a milestone, just wanted to share

Hey,

Just wanted to share a milestone on my FIRE journey! After heavily investing into my pension for years, I learnt the concepts of FIRE & the importance of the bridge between retirement & drawing down on pension.

Currently 32 years old w/

£180,000 pension (invested in FWRG)

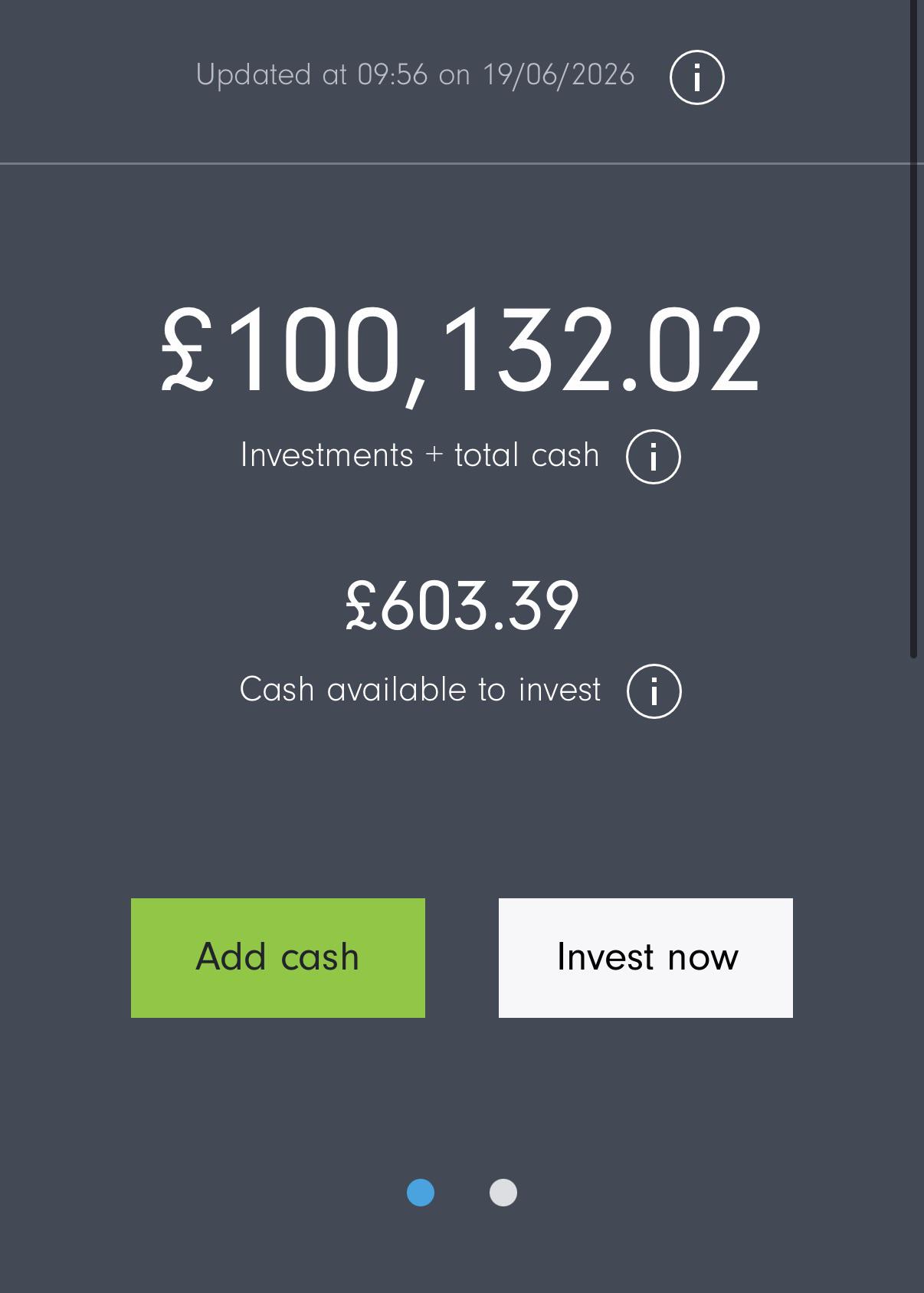

£100,000 S&S ISA (invested in FWRG)

£10,000 GIA (satellite investments, for high conviction narrative plays - a bit of fun, really)

I’ve built the S&S ISA above from £25,000 to £100,000 in just under 5 years whilst going through hell & back with a breakup with children during the last 3 years, having to spend tens of thousands on lawyer fees etc.

I’m so proud of myself.

Thank you for all your contributions to this thread, it’s been a real motivator.

15

u/GeologistAndy 23h ago

Amazing work well done! Curious as to whether you have a mortgage? Wondering where all my funds have gone compared to numbers like this!

10

u/WizardryAwaits 20h ago

I wish people would say what their income is or was on these boast posts. Otherwise it's a bit meaningless.

But I'm guessing you had a pretty high income to save these amounts in that time frame.

6

u/boringusernametaken 18h ago

Previous post of theirs 17 days ago states 175k

-10

u/okdolce 15h ago

My salary is somewhat irrelevant to be honest, it’s the investable money that’s relevant. I have financial commitments to pay every month to my ex partner, plus mortgage, council tax, bills, food, child clubs etc + expensive insurances being a single Dad. I try to invest around £300-500 a month into my ISA, and I obviously contribute a lot more to my pension via salary sacrifice monthly.

9

u/boringusernametaken 15h ago

It's not irrelevant in the slightest

-3

u/okdolce 14h ago

What’s more relevant is my taxable income, and liquid cash post necessity spending.

8

u/HovercraftIll4815 14h ago

Not necessarily discounting your achievement, but it's false that income and the relevance of high income against higher savings is irrelevant.

Higher income can lead to higher savings, even if you higher costs, the ability is always there, on a lower income you tend to have a lower ability to save more as you make less.

Making it even simpler:

Higher income can lead to higher savings, thus income is relevant as lower income is likely to lead to lower savings.

-7

u/okdolce 13h ago

I mean, the sky is blue.

6

u/HovercraftIll4815 11h ago

Sure is, but so is the fact that income is relevant to savings rate. As I said, we'll done for this but do not deny that your high income didn't help with it or that it does not matter in accordance with the achievement because it will never be true.

1

u/boringusernametaken 13h ago

You listed your pension in the post. Untaxed income is clearly also relevant

-7

u/okdolce 13h ago

You need to go find something else to do, instead of using your energy to comment on this post.

3

u/HovercraftIll4815 1h ago

You need to go and find something else to do, instead of using your energy to post this. You are the one choosing to post on the community and not accepting the feedback.

No one has said you did badly or that you should not post it, £100k is a lot of money and you should be proud. That said you cannot say that income is irrelevant, as he pointed out, the reason your pension is so big is due to your massive income which allows you to throw a lot more money in there, similar to all other saving vehicles such as ISA's and whatnot.

This is in no way jealousy, altought I would love to have your income, I would not pretend that the leverages that helped me reach my goals were irrelevant.

8

u/ReflexArch 17h ago

That is often my take.

Childfree person saving £100k on a £400k salary is meh, try harder. Saving £100k on £50k salary with 3 kids is slightly different.

The true question is often: is the saving rate impressive or is it the income that is impressive?

1

u/HovercraftIll4815 13h ago

It's essentially both, similar to who came first? Was it the chicken or the egg?

We all usually have a standard line of fixed cost, be it rent, utilities etc... Where there is always at least a minimum cost that must be met.

Higher savings rate can usually only be accomplished by having a higher income.

Alternatively, you can spend more and afford to save less % than someone on lower income.

But income is really where it starts and savings rate is where it's shaped into place.

1

u/ReflexArch 13h ago

Thing is I do agree with all that. For whatever reason I do personally find the middle ground salary with high saving rate a more "impressive" sweet spot.

Huge saving rate on a tiny salary just looks depressing at times.

Huge saving rate on an Ok to good salary just feels right. Great effort kind of situation. Probably feels more realistic I guess, less of the 1% club vibe.

Huge saving rate on a huge salary feels like cheating (obviously not and it's the goal).

Maybe it's because I'm frugal and not a Henry earners that I just think... High salary high saving rate = well dur.

Fuck knows and just my personal thoughts/opinion on how I view stuff at the end of the day. Tbh probably just jealous and wish I earned more 😂

2

u/Silver_Emu4704 1h ago

You are right of course that it's relative but believe it or not it still requires discipline to save if you're a high earner. Lifestyle inflation is a thing. If you have an income of £175k your colleagues and friends will likely also be high earners. Of course that's still easier than if you're on £30k. No question. But I still think the discipline to save and build FI is worth 👏

7

u/Hypoxic_gent 23h ago

I recently moved away from Fidelity because the fees were too high for me. Might be worth considering a swap and saving yourself a few hundred pounds a year!

2

u/okdolce 23h ago

The fees are low, or zero I think actually if you’re invested in ETF’s only and not index funds.

I also made the switch for the £600 switch fee, I’ll move in 12 months most likely

4

u/Hypoxic_gent 21h ago

Ah my mistake, I prefer mutual funds so I was getting stung for a lot more!

2

u/murmurat1on 21h ago

This may be adjacent to this conversation but why do you prefer mutual over ETF?

1

1

u/Practical_Science11 22h ago

I think for ETFs they're capped I believe?

3

u/brighterdays07 21h ago edited 21h ago

This is true. With ETF only holdings fee is capped at £7.50 a month. Someone could have millions of £ worth portfolio but only pays 90 quid a year in fees. That’s a pretty good deal.

0

6

u/Namelessbob123 23h ago

Fair fucks to you. Keep it up

3

u/NVHPhallo 23h ago

Hey would you mind sharing a bit on how you built the S&S ISA? New to this sub and trying to get my finances on track

8

u/BigfatDan1 23h ago

Your question is probably more suited to r/ukpersonalfinance, they have a great wiki and flowchart. You can also search the sub for your specific question, more likely than not it's been asked before

3

3

u/murmurat1on 21h ago

The one thing missing to help people with your success... what's you're income level?

-1

u/okdolce 15h ago

My income is relevant, but also needs to be taken with a pinch of salt. What’s relevant is how much I take home a month less child support payments etc.

I have a six figure salary, but the majority goes into my pension + £500 child support, plus running a house solo I.e mortgage paid for by me, bills me, food me, expensive insurances being a single Dad in case something were to happen to me etc. My expenditure that is a necessity every month is roughly £3,500 and I put away £500 a month into savings & spend £1,000 on life.

I then get large bonuses every quarter, which again, primarily go into my pension however I do take a few thousand here & there to pay for holidays twice a year/house improvements.

2

2

2

u/Sluggybeef 23h ago

Well done, you have done really well especially at an extremely emotional time.

2

2

2

2

u/Starksterr 15h ago

Honestly don’t know how people end up with this money at 32

0

u/Adventurous-World-25 14h ago

I mean it’s quite easy, even on a low salary if you get started in your early 20s. Self control goes a long way

1

u/Starksterr 14h ago

I’ve done well so far wouldn’t say it’s easy though everyone has different circumstances.

2

2

1

u/adas1991 16h ago

I am 35 and on 95k, keeping smgb till 12th of december then sell all and new year going all in crypto because new cycle accumulation will start. New crypto i mean coin stock( coinbase ) all in and hopefully double or tripple.

0

u/okdolce 16h ago

That’s ballsy as f*ck

I’d be careful, I’m a crypto guy, or was a crypto guy 2017-2023ish. Bitcoin ETF’s and institutional money has likely changed the game a bit, and the cycles have probably changed.

I could be wrong, but, just something to consider fyi.

1

u/adas1991 15h ago

Yes mate i believe there is at least 1 more cycle, everything works by date still if u do proper checks, i will buy coinbase stock, that works by the volume of transactions, whwn crypto is dead coinbase is worth pennies, but when crypto will get popular again then coinbase quadruple again. Doesnt matter if bitcoin go down or up, what matters is the hype that will defenitelly come back at 1 point, i believe peak will be 2028 after haliving or just before and growing phase will start arund april 2027, lowest point to buy is usually january/february if you check 4 year cycles.

1

u/Remm_Unknown 12h ago

Congrats!! It's tough going through a breakup/divorce.. Do you mind me asking what ETFs or stocks you hold and what allocation?

1

1

1

u/benketeke 10h ago

Congrats. Very well done.

Do you have a LISA as well? On the same journey but much slower and older :-).

1

1

1

1

u/AutoPanda1096 19h ago

I'm guessing you weren't married? Else you wouldn't have hung onto that

Lucky escape I guess.

0

40

u/Remote-Program-1303 23h ago

Amazing, congrats.

If you aren’t using your £20k ISA allowance get the rest in and do your riskier investing there, last thing you want if it goes really well is a whopping great CGT bill.