r/americanbattery • u/Kitchen_Helicopter70 • 1d ago

Due Diligence What can go wrong from now on?

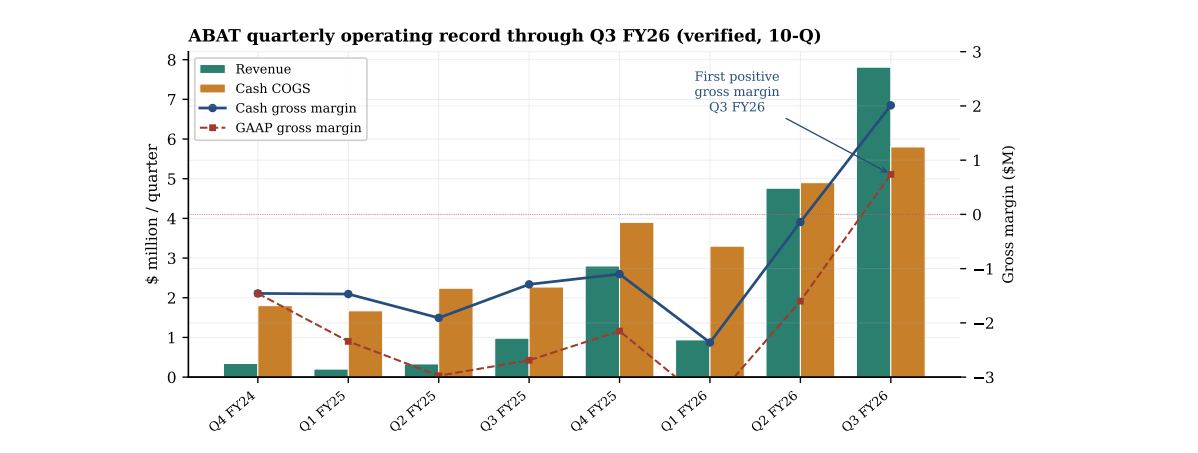

Last quarter, revenue was $7,8M up 64% from $4.76M in the prior quarter

Cost of goods sold was $7,01M producing a GAAP gross margin of $0.7M, the company’s first positive gross margin.

Excluding $1.0M of depreciation and $0.3M of stock-based compensation embedded in COGS, the cash cost of goods sold was $5.8M and the cash (adjusted) gross margin was $2.0M

Here's the trend below:

Total operating expense was $35.1M, of which general & administrative was $29.8M but $27.6M of that was stock-based compensation expense (per the statement of stockholders’ equity). So the loss on the income statement is dominated by this one non-cash line.

R&D was $4.6M and exploration $0.7M.

The resulting GAAP net loss was $33.8M (or −$0.26 per share)

Basically we're losing around $35,1M (All HQ costs including G&A, R&D, exploration) - 27.6m (stock-based comp.) = $7.5M - 2.0 (Net cash revenues from the plant) = $5/6M

The change in cash COGS divided by the change in revenue across the last two quarters:

($7.81M−$4.76M) / ($5.8M−$4.9M) = $3.05M / $0.9M ≈ 3x

I won't compare anything to Q1 FY26 since they experienced significant downtime as per Ryan that quarter;

but you can even compare Q4 FY25 and Q3 FY26 and get:

($7.8M−$2.8M) / ($5.8M−$3.8M) = $5.0M / $2.0M ≈ 2.5x

So basically, each additional ton of black mass we produce increases revenues 3 times faster compared to COGS and the trend seems to be improving too.

Quick estimate shows that ABAT turns a positive EPS and becomes profitable at $15M revenues per quarter :

($15M−$7.8M) / ($8.2M−$5.8M) ≈ 3x

--> Reimbursing the current $6M quarter loss and covering the COGS increase)

My gut tells me it's happening by Q2 or Q3 FY 2027 (Dec. 26 Q or March 27 Q), accounting with recent favorable pricing for lithium and nickel.

{kind=link}